Market Analysis

Assessing the resilience of Saudi manufacturing in 2020 and beyond

Global April 11, 2021 - By

As we emerge from the pandemic economy, some sectors are rebounding faster than others.

In 2020, the COVID-19 pandemic sent shock waves through the Kingdom, shutting down large segments of the economy as manufacturing businesses (and other sectors) were forced to scale back. But at the beginning of 2021, there are clear signs that a recovery of the Saudi economy is under way.

Aramco’s Strategy and Market Analysis (SMA) explores the manufacturing sector’s performance in 2020 through the lenses of three main regular frequency indicators available: The General Authority for Statistics’ (GASTAT) industrial production index, export volumes, and cement sales, all serve as indicators for the speed, breadth, and shape of the recovery.

Production

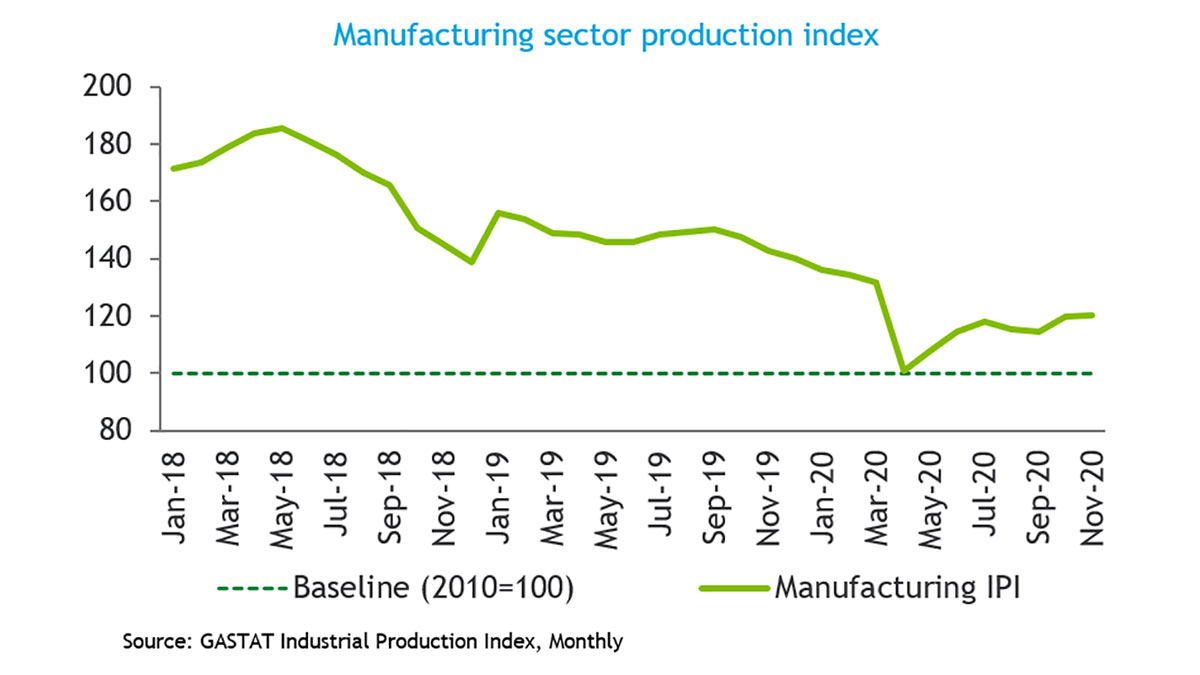

The Kingdom’s industrial production index, published by GASTAT, assesses relative changes in the monthly volume of industrial output compared to 2010 (reference year). The overall index covers manufacturing, mining/quarrying, including oil and gas, and utilities. It is also based on a monthly survey of over 3,000 industrial establishments.

Between March and May 2020 (with the COVID-19 lock down in effect), manufacturing production fell to a decade low as shown in the adjacent chart. It has since risen as the economy has gradually re-opened, but remains much lower than historic trends.

Beyond COVID’s impact in 2020, the general decline since 2018 reflects the slow recovery from the lower oil economy and other structural changes that have been underway for a while. Nevertheless, the sector has mounted a recovery and is now trending higher each month.

Exports

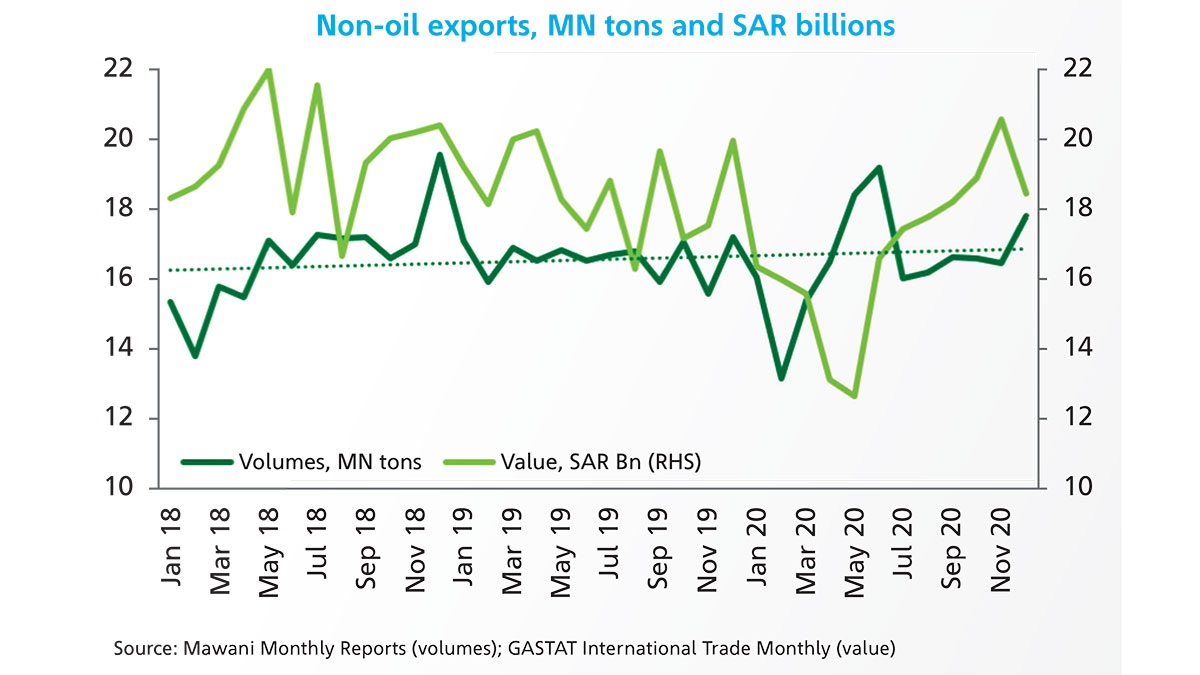

The Kingdom’s manufacturing is dominated by a large export-oriented refining and petrochemical sector, which collectively account for about 50% of the manufacturing sector GDP, 70% of the manufacturing energy demand, and about 80% of the non-oil export volumes. Accordingly, the trajectory of exports since the start of 2020 provides a useful, partial indicator of the health of the sector.

As shown, export volumes saw a dramatic drop early in 2020, but quickly recovered and are now rising. The vast majority of export volumes are in the form of liquid and solid bulk exports (chemicals and refined products) where the Kingdom’s competitive advantages have proven resilient.

Cement sales

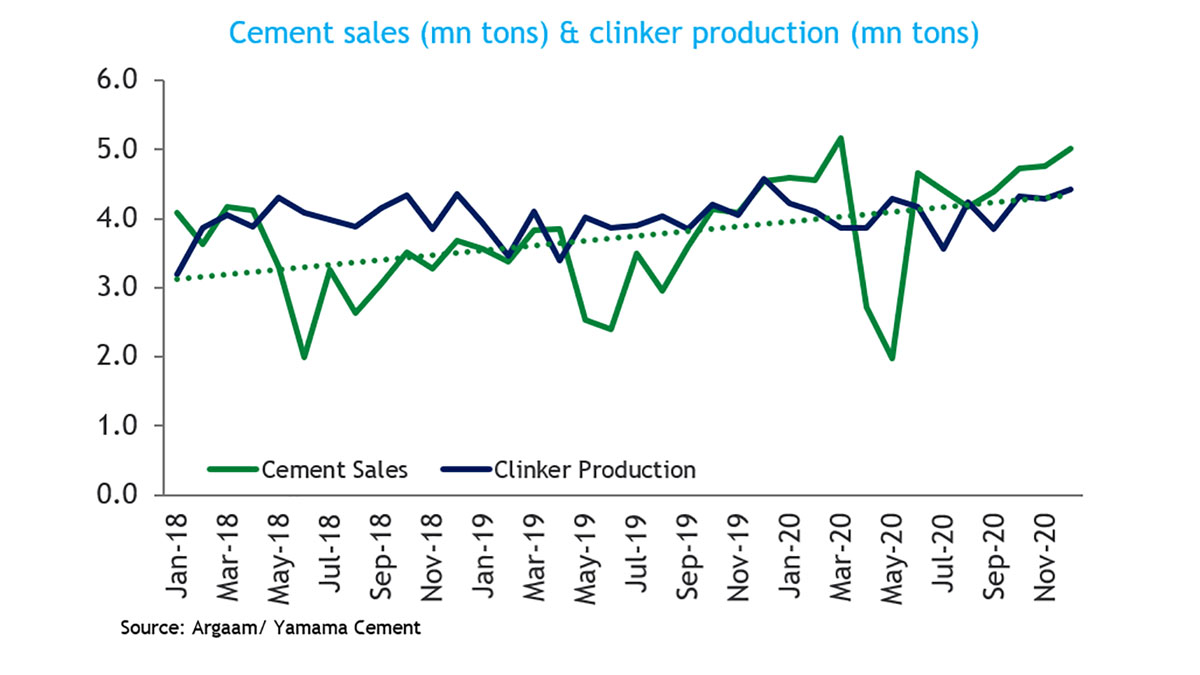

Beyond petrochemicals and refining, the remainder of the industrial sector is primarily domestic facing. This includes nonmetallic minerals such as cement, which accounts for a sizable part of the remaining segments.

Accordingly, domestic sales of cement and production of clinker, an intermediate material in the manufacturing of Portland cement, are a useful proxy for the health of this part of the sector.

As shown, cement sales saw a sharp drop during the lockdown in 2020, but are back to historic highs. This suggests that recovery is now fully underway.

Near term prospects and implications for Aramco

The indicators highlighted suggest that the manufacturing sector has recovered from COVID-19 and is now in growth mode.

Nevertheless, growth in the sector has been stagnant for several years now as seen in the industrial production index, cement sales, and export trend lines shown, and other indicators such as employment, GDP contribution, and export volumes. Therefore, while the rebound has been faster and stronger than in other sectors, the strength of future growth remains uncertain.